Market dynamics, C & I Momentum and Installer requirements

The European solar market is undergoing a remarkable redistribution of installed capacity. While the residential segment has experienced an increase in the energy crisis, 2025 projections at an increasing momentum in the C&I (commercial and industrial) and utility segments indicate. The delay in the growth of homes is mainly attributed to high interest rates, stabilized electricity prices and the phasing out of support regulations such as the Superbonus tax credit of Italy. With 65 GW installed in 2024 and the same (or even less) is estimated for 2025, the European solar market is entering a phase of flat growth.

Source: EUPD Global Energy Transition Get-Matrix ©

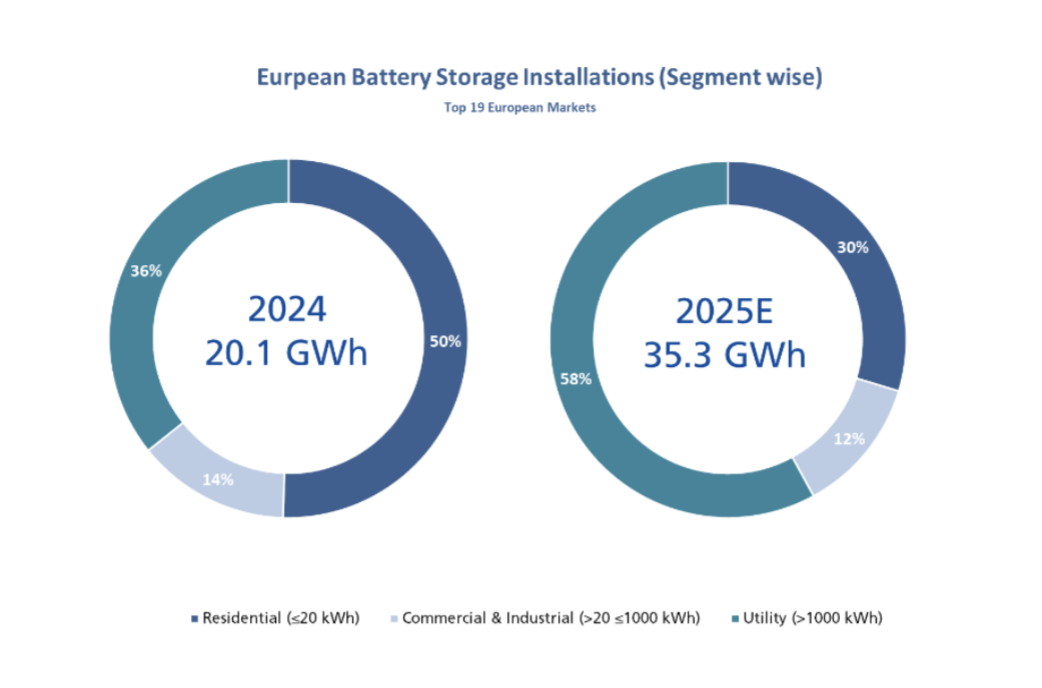

A similar segmental evolution unfolds in the market for electrical energy storage (EES). The installed storage capacity in Europe (top 19 European markets) is expected to grow from 20.1 GWH in 2024 to 35.3 GWH in 2025. The share of the residential storage is expected to fall from 50%to 30%, while the C&I -Segment 12%will represent a slight decrease in the share of the share.

Source: EUPD Global Energy Transition Get-Matrix ©

Such an environment requires urgent attention to two critical developments:

1. The growth of the C&I segment stimulates new investment options and at the same time introduces new risks (tackled in EUPD Research Brand Leadership and Sustainability Rating/BLSR, see here).

2. Innovation has emerged as an important lever for unlocking value, improving margins and building customer confidence, essential factors for attracting new investments, in particular in the residential and C & I sectors.

These trends are clearly reflected in the activities of electric market players. In France, 50% of the installers were investigated in EUPD Research’s PV | Ees Installermonitor © 2024/2025 reported to be active in the C&I segment. When measured at total installed capacity, this share increases to 72%, which underlines the growing relevance of C&I projects. The figures are even higher in Germany. Moreover, European installers have expressed a strong demand for increased innovation; Both developments are investigated in more detail below.

What C&I growth means for manufacturers and investors

The growth of C&I in Europe offers important opportunities, but manufacturers and investors must acknowledge that the continent is a patchwork of various markets, not an united whole. That is why a clear criteria -based uppering of markets based on segmental market -historical and forecast developments, the presence of support regulations, electricity rates and net benefits, etc. is crucial for better results. Without tierization, strategies run the risk of being aligned incorrectly with local realities. Targeted insights make smarter investments and more effective market input possible.

As storage projects are scales in the C&I segment, the risk environment shifts considerably. In contrast to residential systems, C&I installations require larger capital expenses, longer planning cycles and a greater operational accountability. This increases the commitment to selecting reliable technology partners. Fire confidence, satisfaction of the installer, net promoter scores and the possibility to demonstrate persistent R&D investments through patents, certifications and technological resilience: all these serve as the decisive factors. In this context, choosing the right manufacturer is not only about performance or prices, but also about minimizing long -term risks.

To support stakeholders in navigating through these growing complexities, EUPD research introduced the brand leadership and sustainability assessment (BLSR) Framework earlier this year. BLSR is designed to evaluate manufacturers that go beyond financial, price and technical statistics and offers a holistic benchmarking tool that tackles both the needs of investors for brand protection and the needs of the manufacturer for strategic improvement. It makes risk-avoiding brand selection possible via an extensive ESG analysis, including R&D investments, patent-acquisition and installer reputation, which together serve as a risk mitigator for current and future C&I projects.

What do European installers ask for?

Because flat growth in the PV market clearly casts shadow on Ees growth, the majority of C&I and residential installers prioritize innovation. In Belgium, 29%of the investigated installers mentioned product innovation as a critical need, with equally strong reactions in the UK (23%), France (21%) and other markets. The question requires innovation in integration, safety and scalability. As a French installer said: “I would like to see more innovation and better design”; An Italian installation program said that “[they] Would constantly appreciate developments in the seamless integration of inverters and energy storage systems. ”In the Dach region (Germany, Austria and Switzerland) there was a large part of the installer voice for more system integration and smaller system sizes.

Bridging the gap: innovations that meet the needs of C&I installers and customers

While we enter into an energy landscape where C&I storage plays a more central role, innovation is no longer a bonus, but rather crucial to survive. Direct feedback from installers on important European markets consistently points to some common requirements: greater integration between storage systems and inverters, more compact designs, improved safety functions and seamless compatibility with smart energy systems. These requests reflect a growing need for commercial storage solutions that reduce the complexity of the planning and installation and at the same time deliver reliability in the long term.

Recognizing these evolving needs, the EUPD research Top Innovation Awards (TIA) was established to bring the market -ready solutions to the attention that directly tackles the challenges of the installation programs and system integration. Every year EUPD research evaluates hundreds of technology -submissions in solar energy, storage and inverter with an expert jury and installer panel that identifies striking innovations. One of the most compelling TIA recipients are who offer those modular, intelligent and easily too large systems. For example, BYD’s modular storage platform (6–90 kWh) has LFP cells with high density, tool-free installation and smart diagnostics, ideal for space and cost-sensitive projects. Geneedigie’s commercial all-in-one Integrates battery, inverter and EMS with AI optimization in a scalable, plug-and-play format. Wecos 5K0 Smart Emphasizes safety with built -in fire reduction, seismic protection and thermal control in a modular system. The integrated housing system from FOX ESS Combines inverter, battery and EMS in one compact, scalable unit. These innovations simplify the installation, improve performance and interoperability and meet various C&I and residential needs. A win-win for all sides!

Alignment of investor and manufacturer in the C&I Storage

While the European market for energy storage is running to the C&I segment, both investors and manufacturers are confronted with a rapidly changing landscape. Flat growth in PV and storage (usually residential) stimulates a greater demand for precise market targeting via detailed segmental tierization and innovation in system design, integration, operational safety and smart systems: as clearly repeated by installers on the continent. With rising investment risks and technical complexity in C&I implementations, decision -making requires stronger evaluation aids that consider not only technical performance, but also the reliability of the brand, installer and innovation depth. This is the time for the entire PV and storage industry to promote seamless coordination among all stakeholders, especially among manufacturers, installers and prosumers, to unlock win-win results. This is the way!

Authors: Mark AW Hoehner, Varun Mahankali and Ali Arfa

Markus AW Hoehner is the founder, president and chief Executive Officer van Hoeper Research & Consulting Group and EUPD Research. He has been active in research and advice at the highest level for more than three decades, aimed at Cleantech, renewable energy and sustainable management. He can be reached at m.hoehner@eupd-research.com.

Varun Mahankali is a senior analyst and the manager of the Top Innovation Awards at EUPD Research. He has more than five years of experience in clean technical research and advice. His expertise includes market information, innovation analysis and consulting within the renewable energy sector. He can be reached at v.mahankali@eupd-research.com.

Ali Arfa is a senior data manager at EUPD Research. He graduated from the University of Bonn and with a background in European and North American politics. His expertise includes market research, policy development and analysis of stakeholders. His specific focus is on solar energy, energy storage and strategic consultation. He can be reached at a.arfa@eupd-research.com.

The views and opinions expressed in this article are the author, and do not necessarily reflect it by PV -Magazine.

This content is protected by copyright and may not be reused. If you want to work with us and reuse part of our content, please contact: editors@pv-magazine.com.

Popular content