Credit: AES

The American market for energy storage established a record for quarterly growth in the quarter of 2025, with 5.6 GW of installations, according to the latter US Energy Storage Monitor ReporT today released by the American Clean Power Association (ACP) and Wood Mackenzie.

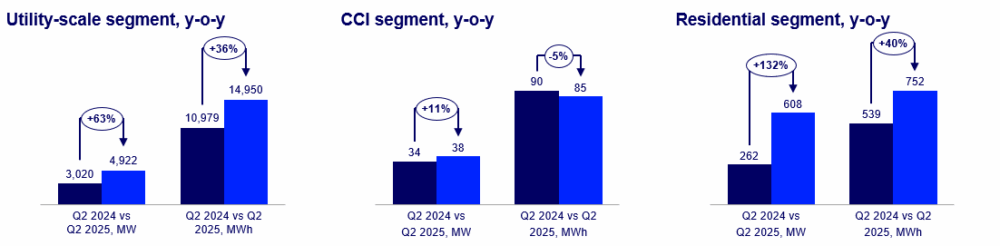

The market for Nuts scale was at the forefront and set up a record with 4.9 GW installed in Q2, sufficient capacity to feed 3.7 million American houses during the average peak demand. While Early Adopters continue to lead in the effort, the activity throughout the country shows a clear demand for energy storage on utility scale as a solution for rising electricity prices and rising energy demand.

- Texas, California and Arizona each added more than 1 GW.

- Markets such as the Southwest Power Pool (SPP) saw renewed activity, with three projects that came online in Oklahoma – the first in the region in three years.

- Florida and Georgia saw major prediction upgrades due to aggressive tenders by vertically integrated aid programs.

“Energy storage is used quickly to strengthen our grid as a demand for power steams and helps energy prices for American families and companies to reduce,” said Noah Roberts, ACP VP of energy storage. “Despite the uncertainty of the regulations, the factors for energy storage are strong and the industry is on their way to produce sufficient schedule batteries in American factories to deliver 100% of domestic demand. Energy storage will be essential for the expansion of the American energy network and American energy production.”

Continue to expand residential and CCI

The residential storage market expanded 608 MW in Q2. This represents an increase of 132% on an annual basis and an 8% jump quarter-over quartaal.

- The majority of growth was powered by California, Arizona and Illinois, because attachment rates achieved new highlights and received systems with a higher capacity market share.

Community-Scale, commercial and industrial (CCI) storage expanded more modestly at 38 MW. This represents an increase of 11% on an annual basis.

- California and New York led Q2 CCI storage installations, accounting for more than 70% of the total capacity, while Illinois got a grip.

- The implementation of the community storage was limited due to high costs and policy restrictions.

Markt shows resilience despite policy uncertainty

According to the report, US Storage will reach 87.8 GW by 2029, powered by segments on residential and utility scale in the midst of a constantly evolving policy environment. However, storage installations on the American utility scale can fall by 10% in 2027, largely as a result of uncertainty compared to the foreign entity of group (FEOC) for battery cells.

“Prices and FEOC uncertainty and slow development of the Community Storage is expected to limit the growth of the CCI segment under 1 GW by 2029, although the Smart 3.0 of Massachusetts can help increase future implementation,” said Allison Feeney, research analyst at Wood Mackenzie. “It is expected that residential storage will surpass solar energy due to a stronger resilience of policy, high attachment rates in important markets such as California and Puerto Rico and continuous ITC access through external property.”

Allison Weis, worldwide head of storage at Wood Mackenzie, said that although the One Big Beautiful Bill Act (OBBBA) kept the ITC for energy storage, the headwind remains and the five -year -old Buildout could be reduced by 16.5 GW.

“After 2025, storage projects in the field of utilities must meet new, stringent battery-sourcing requirements to receive the ITC,” said Weis. “While the domestic cell supply is increasing, the Supply Chain deficits are possible, although developers continue to consider the supply from China to fill in any gaps. A hurry to start construction under the more provisions of the short -term framework ramework raises the forecast in the short term for changing the end of 2025 the risk of the DOWNSTRANN’s Risk is the risk of the DOWSNE Dow’s. Regulations.

News item from Wood Mackenzie