In a new weekly update for PV -MagazineOpis, a Dow Jones company, offers a quick look at the most important trends in the global PV industry.

The Chinese Modulemarker (CMM), the OPIS benchmark for Topcon modules ≥600W, rose 1.18% to $ 0.086/W free-on-board (FOB) China this week, with market indications between $ 0.084-0.093/W. Since the start of the second half of 2025, prices have registered an increase of 4.88%.

Forward curve indications have followed the spot market higher. The prices for Q4 2025 loads rose to $ 0.086/W, while Q1 and Q2 2026 remained stable at $ 0.086/W. Q3 2026 Loads are higher up to $ 0.087/w.

On the domestic market, OPIS rated topcon prices on CNY 0.690 ($ 0.096)/W EXW China, an increase of 0.73% week on week. Sentiment improved after a Ministry of Industry and Information Technology (MIIT) – LED – Meeting, the second in H2 2025 aimed at curbing disorderly competition. In comparison with the session in July, the August meeting was wider, with four important areas: stronger regulation, restrictions on the competition below, stricter quality enforcement and improved self -discipline in industry.

Market speculation is aimed at supervisors who may have established a minimal domestic selling price of CNY 0.75/W ($ 0.096/W FOB China with VAT). If implemented, this would be a deviation from the non-binding cost guidelines issued by the China Fotovoltaic Industrial Association (CPIA), which introduces enforceable legal measures. However, many participants remain careful and doubt the sustainability of such levels in view of the current stock conditions.

CPIA has also called on local authorities to enforce price legislation, to determine minimum bid prices and to reduce the weight of price factors in tenders. The association emphasized rational production tailored to delivery dynamics, as well as quality assurance and protection of intellectual property.

Recent tenders suggest improving sentiment. Huadian Group has awarded a 20 GW module -purchasing for 2025–2026, with topcon bodies on average CNY 0.710/W, while the 3 GW tenders of China Resources Power averages above CNY 0.70/W. These results indicate market stabilization around higher price reaches.

In Europe, the prices of Topcon modules remained stable in the holiday season, with OPIs rating the prices of DDP Europe on € 0.092 ($ 0.11)/W for modules ≥600 W.

HJT products from higher efficiency, however, attract a growing interest despite their price premium, with reported prices at € 0.095/W for ≥600 W modules and € 0.105/W for ≤450 W modules.

Domestic HJT Production Momentum is building. The 3Sun van Enel in Italy already has facilities, while the MCPV of Spain is planting a 2.5 GW HJT factory. Bee Solar and China’s Huasun Energy signed a declaration of intent to develop integrated HJT production in Italy, with operations aimed at 2026.

At policy level, some governments are tightened up. France has shortened tender volumes, while Sweden is planning to lower tax credits, creating a headwind. Nevertheless, new financing and projects continue: the German developer Energiekontor launched a bond of € 15 million to finance solar and wind projects throughout Europe, while Utility RWE 37 MW protected in new solar projects through a federal tender.

In the US, Topcon ≥600W modules DDP US this week 1.44% to $ 0.277/W. The load of Southeast Asia rose by 1.14% to $ 0.267/W after mutual rates, while Indian load fell 1.86% to $ 0.317/W in the midst of a weak question linked to anti-dumping and countervailing obligation (AD/CVD) probes.

Forward Deals for Suggestion Q1 2026 Prices for $ 0.276/Modules with imported cells by WUS-assembled cells are generally quoted at $ 0.30-0.40/W, while with cells with domestic content $ 0.40-0.50/W, with incidental quotes above $ 0.40.

Uncertainty continues around trade and tax policy. The updated Safe Harbor rules of the US Treasury removed the 5%option, but were not used retroactively, calming market problems. Developers rush to secure deals in September before the deadline, so that it remains a short -term company in the short term.

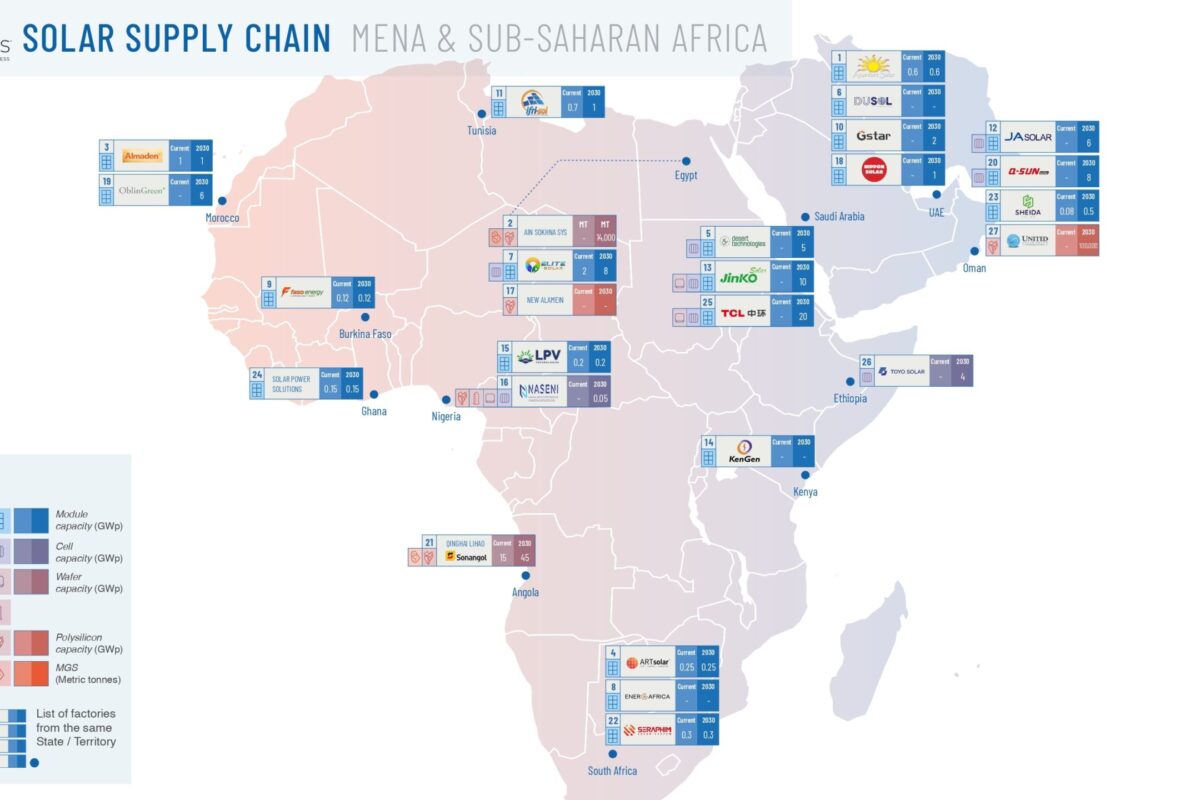

In the meantime, stocks at American assemblers are reportedly shrinking, with one large supplier holding only ~ 100 MW. Of the threatening 2026 restrictions on the foreign entity of group (FEOC), they are expected to create the price provisions between conforming and non-compliant modules. For the time being, opportunistic price increases in connection with new rates are being observed, while Chinese producers are exploring the switching cell production to Africa to circumvent limitations.

The views and opinions expressed in this article are the author, and do not necessarily reflect it by PV -Magazine.

This content is protected by copyright and may not be reused. If you want to work with us and reuse part of our content, please contact: editors@pv-magazine.com.

Popular content