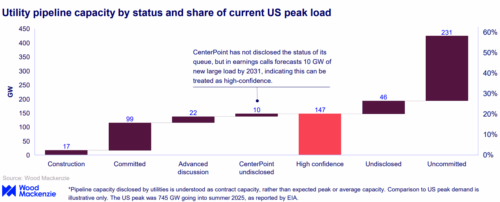

With 116 GW of large loading capacity or under construction, the American utilities are planning a significant growth of large tax capacity-equal to 15.5% of the current American peak demand, according to a new Wood Mackenzie study of important utilities of investors. Accounting projects in advanced discussion or a short -term prediction brings the total to 147 GW, or 20% of the American peak question.

The report, “No way back, an analysis of large loading pipelines with utilities“Shows that a considerable part of this capacity will come online for decade, with 60 GW expected to be added until 2030, similar to 8% of the current American peak demand. Nuts companies expect that 93 GW will be operational by 2035, after which the little pipeline capacity was announced.

“Nuts companies connect to large loads that quickly rage this decade,” said Ben Hertz-Shargel, worldwide head of the edge for Wood Mackenzie. “The market will be difficult to deliver this new tax at that time frame, which can prevent it from happening.”

The report identifies a remarkable shift where large charging projects are placed. While 91% of the current 17 GW of revealed capacity in the matter is located in regulated markets, 54% of the dedicated capacity is not yet under construction and 65% of the capacity in advanced discussion is planned for Deregulated Markets.

Almost three-quarters of high trust load is concentrated in Ercot and PJM areas.

“Capacity not under construction, as well as advanced discussion capacity fall disproportionately in deregulated markets, mainly Ercot,” said Hertz-Shargel. “Deregulated markets are risks of insufficient future offer and price increases for non-large tax customers, who have put forward market interventions from Texas and PJM and will probably ask more in the future.”

Despite a modest increase in the capacity of high trust at different utilities, the share of the total pipeline capacity has decreased in the past quarters, because new requests exceed the progress and withdrawal of existing requests.

Despite a modest increase in the capacity of high trust at different utilities, the share of the total pipeline capacity has decreased in the past quarters, because new requests exceed the progress and withdrawal of existing requests.

“Instead of seeing a trend in the direction of pipeline certainty, we continue to observe the opposite,” said Hertz-Shargel.

The rates of Datacenter increase this uncertainty. The time to reach contract capacity varies considerably for projects of more than 300 MW, often much longer than four years.

“The pace at which utilities connect data centers is only part of the story,” said Hertz-Shargel. “How quickly the schedule actually loads will eventually depend on data center developers.”

News item from Woodmac