The atmosphere at the RE+ tradeshow this week in Las Vegas was generally positive. A challenging nature maintained the first full day of the conference, in which everyone reassuring each other that the sun industry will continue to bloom despite federal policy shifts.

But under that sticky-sweet façade is the truth: some markets will do better than others, and we are still waiting for definitive guidelines for FEOC rules and other construction periods before we know the actual damage. This year there were considerably less residential installers who ran the show than before, (hopefully) because they are extra pressure to close projects before the residential ITC ends at the end of the year. The residential market will be hit hard next year, whereby Wood Mackenzie research director Sylvia Leyva Martinez in 2026 predicts a deterioration of 13%.

I learned that stat and learned more on the research briefing of SEIA and Wood Mackenzie on Wednesday. Research and policy analysts do their best to predict what the American solar industry will look like in the coming years, but that is difficult if things seem to change daily. Here are a few highlights where the groups are confident:

SEIA focuses on the States again policy efforts

SEIA President and CEO Abby Hopper started the briefing by acknowledging that a successful solar industry cannot link its future to federal stimuli that ‘beat back and forth’. Although it still spends time on training federal policy makers, SEIA will work in three areas: 1) first place the energy policy of energy storage, 2) the interests of the state, especially in states with solar supporting governors, and 3) continuous efforts to stimulate domestic production.

With energy storage systems somewhat saved from changes in HR1, SEIA will continue to argue for the technology that is often supplemented with solar energy. Many are also convinced that the stimulas of the state can appear again to stimulate localized solar development. And now “is not the time to run away from onshing,” Hopper said, especially because solar and storage projects of the future need domestic products to meet Dept. of the Treasury rules that the industry does not yet know.

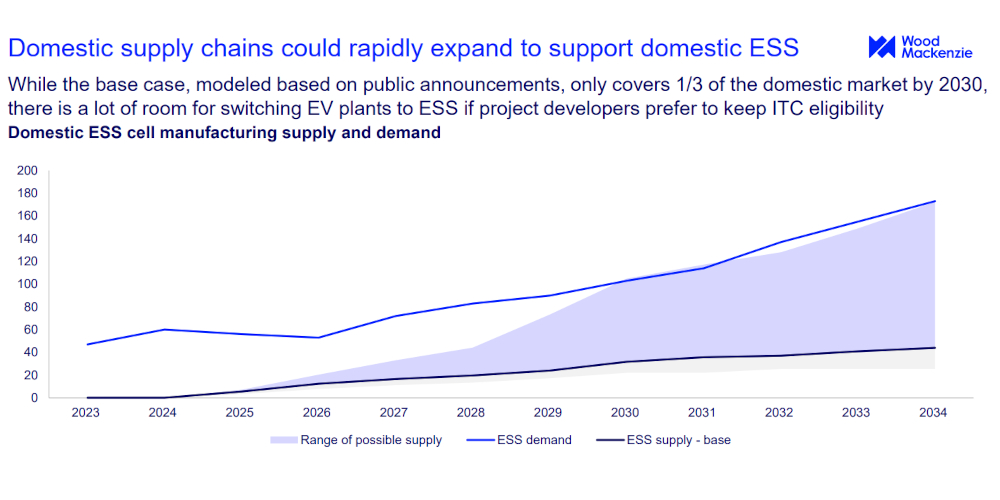

FEOC-compliant storage projects are almost impossible

Although it is still awaiting the final rules, the basic knowledge of FEOC rules is that projects for solar energy/storage that use too many Chinese components are refused federal tax credits. With battery cells that include 50% of the system costs of a BES’s, household battery cells are needed to meet the FEOC threshold. And of course there are very few battery cells made in America, with most of the Chinese companies.

Kasim Khan, Senior Research Analyst from Wood Mackenzie, said it is very likely that energy storage projects in 2026 will not receive the investment tax (ITC) that was extended to the market. But if more EV battery manufacturers switch to the production of cells for the stand-alone storage market, things can change quickly.

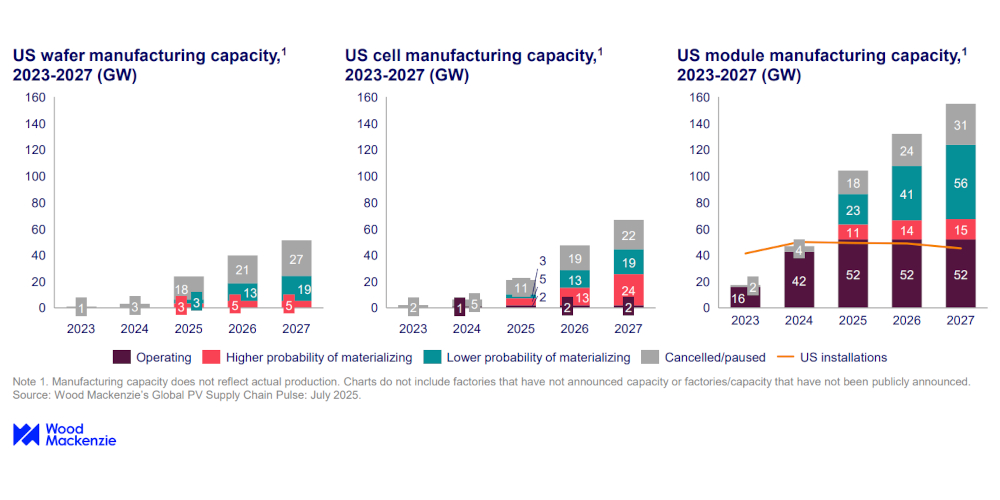

It is unlikely that a self -sufficient supply chain from solar panel will be set up in America

There is more than enough domestic solar panel capacity to deliver the market, but access to electricity components is still missing. With more than 55 GW solar panel assembly currently in the United States, and less than 50 GW is expected to be installed every year until 2030, a stock of American assembled solar panels with foreign components could theoretically meet the country’s requirement. Because projects have found more unique ways to calculate domestic content percentages using balance of system components, less weight is placed on silicon waffles and cells made in America. But it leads to an interesting question, asked by Martinez van Woodmac: Can the United States be confronted for an oversupply situation?

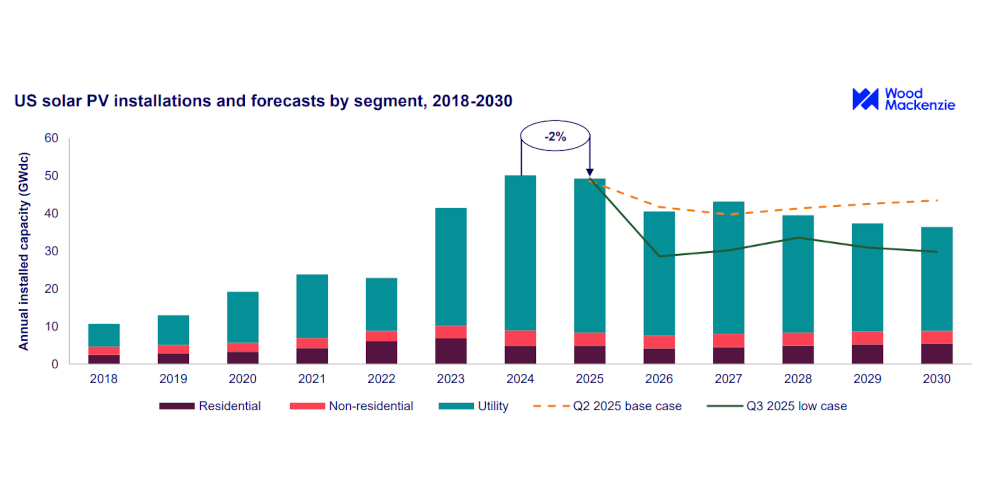

We are already losing projects in 2025

Most solar projects on the utility scale come online in Q4, but Woodmac has already seen a decrease in installations of 24% this year. As soon as the year ends, the group expects to see a 2% decrease in the installed capacity. Although solar projects are still being built, especially since the country needs more rapid electricity to meet the demand for data centers, a dip will feel in the coming years. About 246 GW New Solar – Zon is expected until 2030 – a fall of 21% compared to what was predicted before HR1 struck the industry.

And there are still many unanswered questions. Although a department interior mandate influences solar projects that are laid on public land, the solar sun is still influenced by the delay in approval. If a transmission connection is overtakes public countries, signed projects are stopped. How can that influence large projects throughout the country?

I am completely on board with the RAH-RAH posture in industry optimism and a positive view will take us far. Solar energy is needed to achieve American energy goals, and the question is in all markets. SOld Power World Will stay here to search the latest policy developments that it will all happen.