Solar Media Market Research analyst Josh Cornes provides an overview of operational solar capacity in Britain, which, despite some of the barriers developers have faced this year, continues to rise at a healthy pace.

Overall, 2025 can be seen as a success for the solar industry. Grid reform will pave a path in the coming years, and the capacity going live is at levels not seen in the last decade. Britain has now reached 14 GWp of operational capacity for utility-scale ground-mounted solar, and the market continues to grow year on year.

Last year exceeded expectations by approx 1.3 GWp of utility-scale ground-mounted solar goes live.

This was greatly helped by the significant rush towards the end of 2024, with the fourth quarter being the busiest quarter since 2016. One developer completed three sites within weeks of each other, totaling 150 MWp.

By the beginning of this year, Market research in the field of solar energy predicted that UK ground-mounted solar capacity will increase by around 80% year-on-year. This remains the case: almost 2GWp has now gone live and another 2GWp started construction over ten months ago. With an average construction time of between 50 and 70 weeks for a 69 MWp location, a further realization of 500 MWp is certainly possible this year.

The second quarter was huge for 2025, with the most capacity going live in a single quarter (900 MWp) since the Q1 2016 incentives. This included the first Nationally Important Solar Infrastructure Project (NSIP) to be completed: Cleve Hill Solar Farm, the 373MWp project owned by Quinbrook Infrastructure Partners, built by Metlen. Some other notable projects included Worset Lane Solar Farm (69.9 MWp), Bunkers Hill Solar Farm (66.5 MWp) and Birch Solar Farm (69.9 MWp), all projects at the top end of the local planning authorities’ capacity range.

Figure 1: Operational capacity in Great Britain broken down by year and quarter, outlining year-on-year improvements since 2017.

Figure 1 highlights the bump at the end of 2024, which could allow operational capacity to grow significantly year-over-year. It also outlines the successful first half of 2025, while the third quarter was relatively quiet. This may be due to the fact that the power grid reform diverted a significant part of developers’ attention from the construction of their projects. The fourth quarter is generally a busy quarter in terms of deliveries; approximately 550 MWp will be operational in the fourth quarter of 2024.

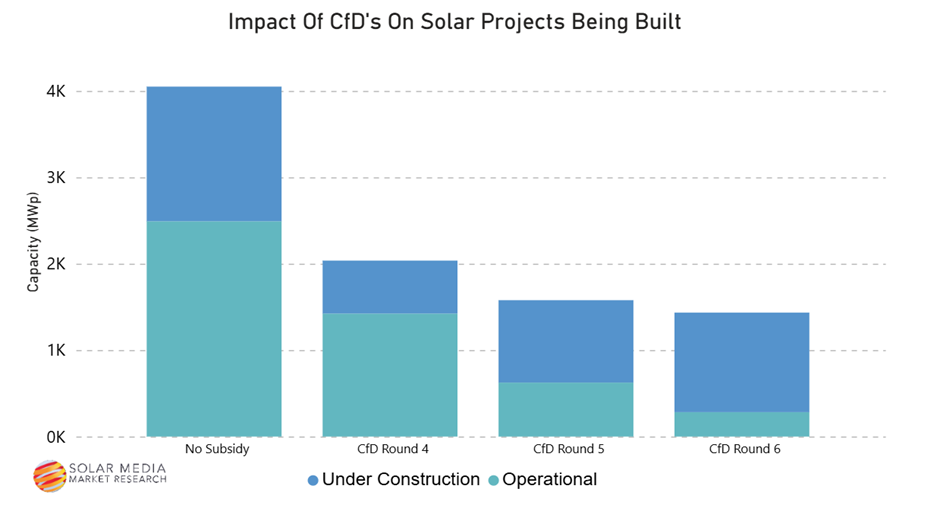

Contracts for Difference (CfDs) remain essential to the growth of the UK market. Figure 2 shows that more than half of the capacity completed or under construction in the last four years has a CfD. From allocation round 4 (AR4), 75% of the awarded projects are now in this phase. Of the 700MWp from AR4 that still needs to be built, one developer has more than 400MWp.

Figure 2: CfDs remain crucial, encouraging developers to build projects within three years of receiving their contracts from the government.

AR5 projects are also moving in the right direction: more than half of the allocated capacity is under construction or completed.

In AR6, 93 locations received a CfD, totaling 4.5 GWp. More than a third of these have already broken ground, with some developers who have acquired multiple projects looking to complete their portfolio within the next twelve months.

With the M&A market at record highNumerous projects that have changed ownership have previously secured CfDs, and developers are currently tendering and construction will begin soon.

Britain is moving in the right direction, with strong year-on-year growth. Next year will be a fantastic year, with more than 4GWp under construction. If developers can get the green light for their secure connectivity projects, this year could break records.

All the data above comes from Solar Media Market Research analysis, which can be accessedhere.

Send an email to book a demo and access the data[email protected].