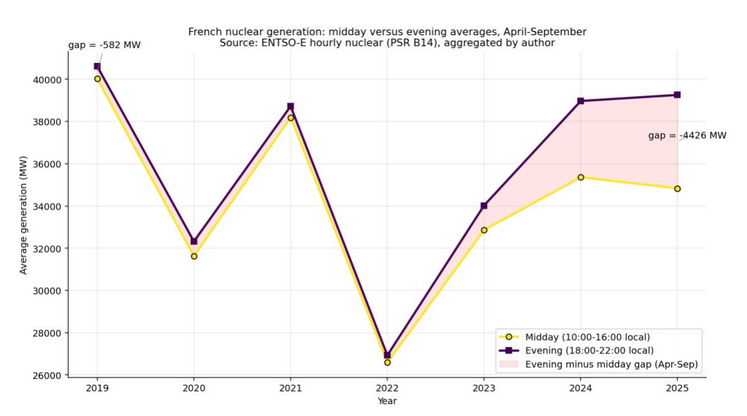

For most of the last forty years, French nuclear power has been the closest thing Europe had to a true baseload backbone. The reactors were shut down all day, causing production to drop only at night, when domestic demand was lowest. Hourly data from the ENTSO-E Transparency Platform shows that the pattern has reversed. Between 2019 and 2025, the average fluctuations between afternoon and evening production over the period from April to September grew from 582 MW to 4,426 MW. That’s almost an order of magnitude. During the hours when European solar energy is at its peak, the French reactors no longer behave as base load.

Nuclear modulation in France, where reactors are operating below their maximum capacity, reached 33 TWh in 2025, more than double the 15 TWh recorded in 2019. The shift is unambiguous in both the annual totals and hourly flows. The daily price form that Europe has predicted for the late 2020s has already arrived in France.

An order of magnitude change, year after year

The graph below shows the full-year daily averages of French nuclear production, solar generation, total load and net exports for three reference years: 2019, 2023 and 2025. The nuclear curve for 2019 is flat throughout the day. The 2023 curve is lower, with the fleet still recovering from the maintenance outages caused by the stress corrosion of 2022, and is only slightly concave. However, the 2025 curve is unequivocally concave. It shows a clear afternoon dip compared to the morning and evening levels. The same panel shows the reverse on the solar side. The 2025 solar curve peaks at precisely those midday hours, and the 2025 net export curve peaks at the same time, when the rest of Europe absorbs the surplus.

Image: Ricardo PLC

Leave out winter, when there is little solar energy, and the signal becomes sharper. From April to September, the gap between average French nuclear production in the afternoon window (10am to 4pm local time) and the evening peak window (6pm to 10pm) grows from 582 MW in 2019 to 4,426 MW in 2025.

Although the data for the first quarter of 2026 are not directly comparable with the summer figures, they already show a difference between the afternoon and the evening of approximately 2,500 MW. That’s big for winter in northwestern Europe, when solar energy is at its annual minimum. The change between 2022 and 2025 cannot be explained by maintenance planning. The 2022 dip reflects the stress-corrosion crisis, but the gap widens every year after that.

Image: Ricardo PLC

The shift consists of two components: a larger annual modulation volume, and a change in the time of day at which that modulation occurs during the day. Previously, the fleet shrank at night, caused by lower domestic cargo. It now dips around noon and into the afternoon, caused by high levels of European solar power generation. The price side tells the same story. What used to be an afternoon plateau for French wholesale prices is now an afternoon trough.

Economic dispatching, no capacity limitations

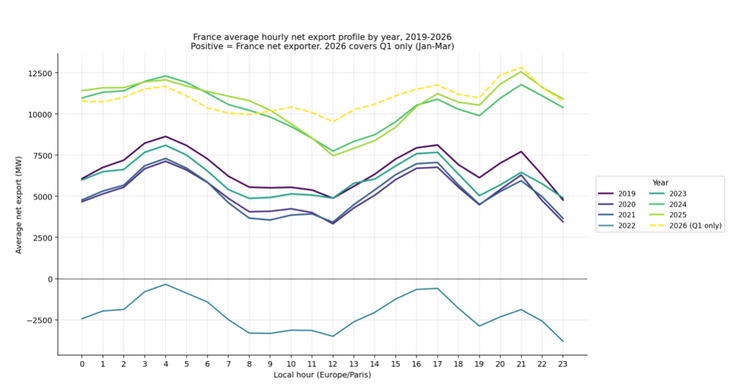

France was a net exporter in 98.5 percent of the hours in 2025. The annual export balance amounted to 92.3 TWh, the highest ever measured and comparable to the annual electricity consumption in a country such as Belgium. The fleet is not undermanned because it has nothing to produce.

What changes is the marginal decision in the hours when the fleet is not empty. In the 129 hours of 2025, when France was a net importer, French nuclear power averaged 8.7 GW below the annual average. The equivalent difference in 2024 was effectively zero. Import hours no longer indicate scarcity at home, but rather cheap sustainable surpluses abroad. The average import price over the 2025 import hours was 33 euros per MWh, the lowest since the markets opened, and about half of those hours were at negative prices.

For anyone modeling French nuclear margins based on 2019 price form, the inversion is fundamental. An import-related hour for France used to be an hour with high prices, driven by domestic scarcity. In 2025 it will be a time of low prices, driven by foreign abundance.

Image: Ricardo PLC

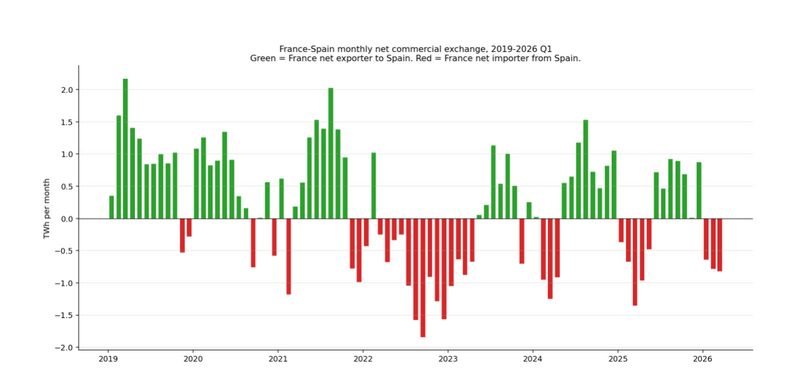

The Spanish border appeared first

The clearest cross-border picture of the shift is Spain. Until 2021, France was an almost permanent net exporter to Spain. The 2022 nuclear crisis reversed that, with Spanish exports supporting France until early 2023. Since 2024, the balance has been almost zero, only 0.2 TWh net in 2025, consisting of 7.6 TWh French exports against 7.4 TWh imports.

What matters is when the net export months appear. As illustrated in the graph below, they cluster in 2024 and 2025 in February to April, the months when Spanish solar energy is already producing substantially, but Spanish demand for summer cooling has not yet increased. That is the temporary fingerprint of the solar saturation in the bidding zone. It has appeared in the Spanish zone before Spain has reached the installed capacity that several other European markets are targeting for 2030.

France does not export less because it produces less. The country exports less because Spain has cheaper electrons for hours. The same dynamics will occur at any border where solar penetration exceeds local storage and demand flexibility on the other side.

Image: Ricardo PLC

The Italian border still looks like the Spanish border circa 2018. France exported a net 26.2 TWh to Italy in 2025, with Italian wholesale prices averaging 116 euros per MWh, compared to 61 euros per MWh in France. The Italian generation mix remains gas-rich. Whether this will remain the case as Italy’s solar capacity grows is one of the truly open questions for the second half of the decade.

What to watch…

Three things we need to monitor in the coming years.

1. Will the Italian border start showing Spanish-style imports into France early in the spring? The Italian solar capacity, the gas price and the battery composition are the variables. The Spanish precedent shows that the turnaround can happen quickly once conditions align.

2. How is French nuclear modulation growing as a percentage of fleet production? The 33 TWh of 2025 is approximately 9% of the total French nuclear generation of 373 TWh. The nuclear fleet has not yet experienced double-digit modulation as a share of annual production.

3. How do German solar forms cross transboundary currents? As Germany’s solar fleet continues to expand rapidly, periods of cheap solar generation are already changing commercial energy flows in the region. As more renewable capacity comes online, these impacts are likely to increase, with potential direct and indirect implications for the modulation of nuclear production in France.

Author: Safa Sen, Market Engagement Lead for CWE at Ricardo, member of WSP.

Ricardo is a member of the professional services firm WSP Group, which unites technical, consulting and scientific expertise to shape communities and advance humanity. From local beginnings to a global presence today, it operates in more than 50 countries, providing solutions and delivering innovative projects across sectors: transportation and infrastructure, real estate and buildings, earth and environment, water, energy and mining and metals.

How Ricardo’s electricity market prospects can help

How quickly does your bidding zone follow Spain into midday saturation? When will negative price hours start eating up the capture rate of your assets, and by how much? Which CfD strike price will hold if the merit order is revised hour by hour by neighboring solar?

Ricardo’s Electricity Market Outlook (EMO) was developed to answer these questions. The underlying model, PRIMES-IEM, underlies twenty years of policy analysis by the European Commission. It manages all European markets simultaneously until 2050, deriving cross-border flows by replicating the EUPHEMIA algorithm used by ENTSO-E.

The outputs include hourly prices, capture rates, depth and frequency of negative prices, exposure to curtailments and BESS profitability forecasts at country and asset levels. These are the quantitative inputs that CfD bidding prices and project bankability matters require.

The views and opinions expressed in this article are those of the author and do not necessarily reflect those of the author pv magazine.

This content is copyrighted and may not be reused. If you would like to collaborate with us and reuse some of our content, please contact: editors@pv-magazine.com.

Popular content