Solar Media’s UK & Ireland Portfolio Lead Analyst Josh Cornes maps the capacity that will probably be online by 2030 after reforming the network connections in the UK.

The hurry to take projects online to contribute to the government’s objective of the government 2030 is in full swing.

Developers have submitted their projects to the National Energy System Operator (NESO) in the hope of obtaining the coveted Gate 2 Grid Connection offers, after having spent months with ‘strategic coordination’ with the clean energy plans of the VK as set out by NESO in November 2024.

Although there is a feeling among the community Reform of the grid connection can be rushedWith countless supervision along the way it was clearly one Revision of grid was required To move forward.

The previous system saw some projects given schedule connection dates up to 12 years after entering the planning system; Developers hope to raise such connection offers with up to 10 years under the new process.

Planning is one of the most crucial things in proving strategic coordination, because this is the best way to emphasize project willingness and that construction will begin in the near future.

Figure 1: Export capacity is exported, in planning or operational compared to the Clean Power 2030 allocated totals per DNO, according to the Solar-Solar: UK Pipeline database of Solar Media.

Figure 1 outlines the capacities assigned by Neso per DNO against the projects that are currently written or improved.

This is what I will count if the “queue” below, with the exception of the projects with grid connections, but in no way must claim. Such projects can be too early phase to be feasible or moths (referred to as ‘zombie projects’).

The first thing we notice is the over -promotion in some regions compared to the headroom that is seen in others.

Take Northern Power Grid as an example, where Neso has assigned 4.4 GW. According to Solar Media’s Market Research There is currently 600 MW connected, with another 5.3 GW or scoped, in planning or under construction. This goes much further than the assigned 4.4 GW, so that developers in a very early stages are given in a very early stages, little hope to get gate 2 offers.

Conversely, UK Power Networks (UKPN) has assigned the largest headroom, with 8.1 GW and only 7.3 GW currently scoped or further demanded.

One reason for the important target in this area is the size of the population, which leads to an increased question. However, there seems to be a lack of infrastructure, with almost all 7.3 GW shown in Figure 1 that is currently contracted to connect to only 20 different grid supply points (GSPs). This includes Bramford, which has the largest queue (more than 1 GW) of each GSP in the UK. Walpole, who has the third largest queue (800 MW), is also in this region.

Similarly, the lack of infrastructure concerning in East Sussex and Kent. Both have an enormous amount of green space, with a complete lack of GSPs. In these two provinces, only 1 GW of projects on scoping of Futher, less than the capacity only in Bramford.

As mentioned above, these figures do not include the projects that should not progress in any way. When we throw it in, it tells a slightly different story, with more than 13 GW solar energy with a contract with UKPN.

This means that 6GW of these projects still have to be found or the British planning system is affected. Figure 1 shows that there is hope for some of these projects, but these developers will have to move quickly if they want to protect the grid connections from before 2030.

Scotland starts to grow, but walks far behind England and Wales

Scotland has only been assigned a maximum of 3.7 GW, just over one tenth of the distribution capacity assigned by Neso for the reform of the network.

This is no surprise, with barely 400 MW operational in the region. However, the pipeline has grown considerably, where 1.2 GWP was submitted in 2025, more than any other year earlier.

Although Scottish Electric has the lowest solar goal in the UK and the lowest operational capacity, it has the largest queue, approved with more than 800 MW and 140 MW under construction.

You can take the above sentiments and apply them to each DNO to paint a picture of the queue per DNO.

Projects that enter the planning system, as expected, are all high. Figure 2 emphasizes the impact of the deadlines set by Neso, in particular the Gate 2 -intervention window that was originally expected to close at the end of July.

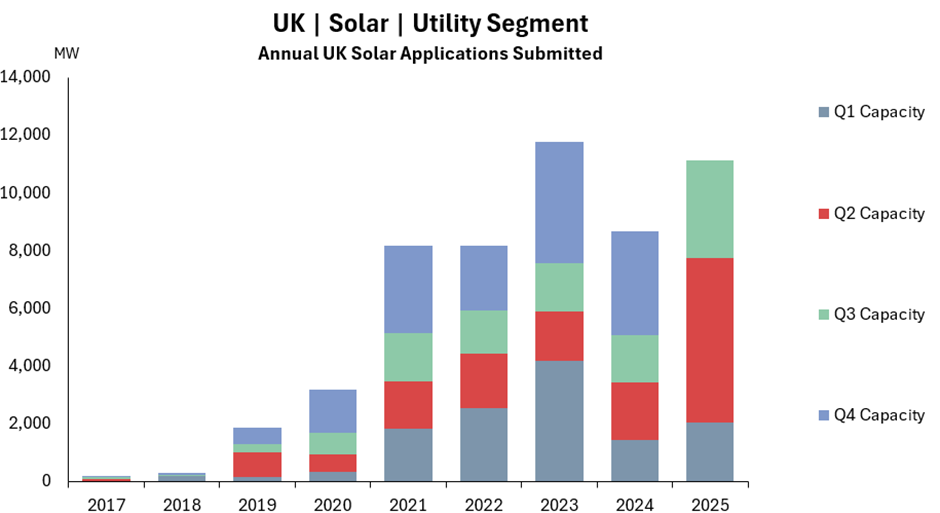

Figure 2: UK Solar Planning submissions in the past 8 years demolished per quarter, with 2025 almost all years in the first 8 months surpassed.

July had submitted the highest capacity in history, with just over 3GWP, a huge number, since only 2 months earlier had 2GW, December 2024 and June 2025, both very important months in the context of CP30.

All data and analyzes shown above come from the analysis of Solar Media Market Research, which is accessible here.

Contact the in -depth data used in Figure 1 [email protected].