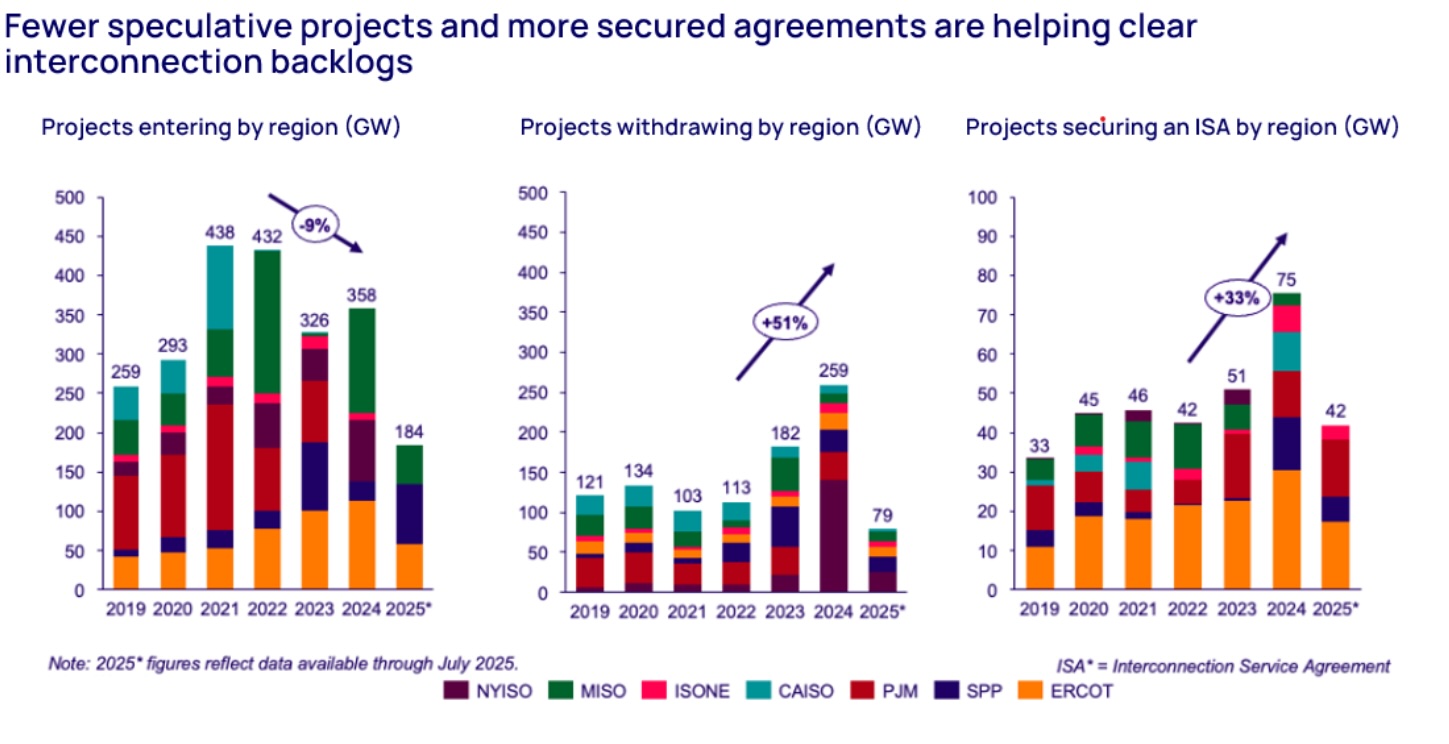

United States Grid -Interconnection agreements reached historical highlights in 2024, and rose 33% to 75 GW – the highest volume ever – due to new federal regulations aimed at streamlining the process, according to a new report from Wood Mackenzie.

According to the report “Following the progress of US -Sraster -interconnection”, “ Data from the Lens Power and Renewables platform of Wood Mackenzie shows that the Federal Energy Regulatory Commission (FERC) Order no. 2023, issued in July 2023,, together with other reforms led by independent system operators (ISOs), had a significant impact on the processing of interconnections -transmites about the processing of interconnections -transverse meetings Through speculative projects and CLARE -CREHEER.

On top of increased connections, regional raster operators experience 9% fewer new project listings, an increase of 51% in recordings of non-living projects since 2022.

“It is clear that these reforms show early signs of promises when accelerating the pace of interconnection studies,” said Kaitlin Fung, research analyst, North America on Utility scale solar zonne energy for Wood Mackenzie. “We saw a record year in 2024, with 75 GW secure capacity. 2025, this momentum maintains this momentum, because large grid operators have already protected 36 GW until July 2025, which corresponds the year the record of 2024.”

Solar and Storage continue to dominate secure interconnection agreements

Solar and storage technologies conquered 75%, or 58 GW, of all interconnection agreements in 2024 and will retain a similar market share in 2025. Solar has been half of all signed IAS since 2019, a trend that will take place in 2025.

Natural gas has seen an increase in interconnection requests since 2022, which adds 121 GW capacity. This trend continued in 2025 with new applications for gas generation that break the annual archives already halfway through the year. However, the number of successful gas connection agreements has fallen by 25% since 2022, mainly in PJM, Miso and Ercot.

Regional differences

“Interconnection success and waiting operating times vary dramatically for various grid operators in regions,” Fung said.

According to the report, Ercot leads both in the success rates and in the processing speed due to the streamlined queue process through their connecting and managers approach. Isone is in second place in the success rate, but has the longest processing time due to the delayed transition from serial to cluster -based processing. Caiso is in third place, but has one of the lowest success rates, powered by a large volume of speculative projects.

“Although we see a positive momentum, there are considerable challenges,” Fung added. “Natural gax projects go at record levels in row, but since 2022, annual interconnection contracts signed, and regional differences in processing times emphasize the need for continuous reform efforts.”

News item from Wood Mackenzie