The escalation of conflict in the Middle East is once again exposing the fragility of global energy systems, where disruptions in key transit routes such as the Strait of Hormuz, responsible for nearly 20% of global oil and gas trade, are driving volatility in oil and LNG markets. For Europe, which remains structurally dependent on imported gas and LNG, this translates directly into renewed exposure to price shocks and supply uncertainty especially in more dependant European markets. These developments reinforce a broader structural shift already underway: energy security is becoming a central driver of investment decisions, particularly within the commercial and industrial (C&I) and utility segments, accelerating the adoption of solar and storage as reliable, domestically controlled energy solutions.

At the same time, this demand-side acceleration is coinciding with a rapid expansion of global manufacturing capacity, particularly in China and gradually in India, where supply is far exceeding domestic absorption. With access to the United States constrained by tariffs, origin requirements, and regulatory frameworks, Europe is emerging as the primary export destination for this growing surplus. As a result, the region sits at the intersection of strong renewable demand and rising global supply, setting the stage for a more competitive and increasingly selective market environment.

From Crisis Response to Europe-Centric Energy Transition

This trajectory follows a familiar pattern. After the disruption of Russian gas supplies, Europe accelerated renewable deployment through initiatives such as REPowerEU, with solar and storage installations rising sharply, particularly in the residential segment. The current geopolitical environment is reinforcing this transition, but with a shift in structure. What began as a policy-driven and consumer-led response is evolving into a system-level transformation, where energy security, price stability, and resilience are central to investment strategies.

Across regions exposed to fossil fuel imports, solar and storage are viewed as immediate and scalable solutions, offering faster deployment and more predictable costs than conventional energy infrastructure. Within this shift, Europe stands out due to its sustained demand, policy alignment, and continued exposure to external energy risks, reinforcing its role as the primary market where global demand dynamics are taking shape.

Europe at the Center: From Residential Surge to System-Driven Growth

Europe’s solar and storage markets continue to expand, with growth being shaped by energy security priorities. Following the disruption of Russian gas supplies, the EU-27 along with the UK and Switzerland saw a sharp rise in residential solar installations, with annual PV additions increasing from around 31 GWdc in 2021 to nearly 68 GWdc in 2023 as households responded to price volatility and supply concerns.

At the same time, a structural shift toward commercial, industrial, and utility-scale deployments has already been underway across the European markets (read more). The current geopolitical environment is reinforcing this transition, as businesses and energy-intensive industries accelerate investments in solar and storage to hedge against price volatility, secure long-term energy supply, and meet decarbonization targets. According to the EUPD Global Energy Transition (GET) Matrix©, annual PV installations are expected to stabilise at around 70 GWdc in 2025–2026 before gradually rising toward nearly 78 GWdc by 2028, with a growing contribution from larger-scale systems.

This shift is even more pronounced in the storage market, where total capacity is projected to grow from approximately 31 GWh in 2025 to over 50 GWh in 2026, reaching around 85 GWh by 2028. While residential storage expanded alongside rooftop solar in the earlier phase, current growth is increasingly driven by commercial and industrial (C&I) and utility-scale applications. In particular, C&I storage is emerging as a critical enabler for energy cost optimisation, peak shaving, and operational resilience, reinforcing its role as a key growth segment within Europe’s evolving energy system. Survey responses from the new EUPD PV & Storage C&I EPCMonitor© 2026 indicate that electric mobility is already a standard component of C&I offerings, with around 59% of active EPCs already deploying EV charging infrastructure.

As a result, the European market is becoming more value-driven and system-focused, where performance, reliability, and integration are now as important as cost considerations.

Europe as the Primary Destination for Global Solar & Storage Supply

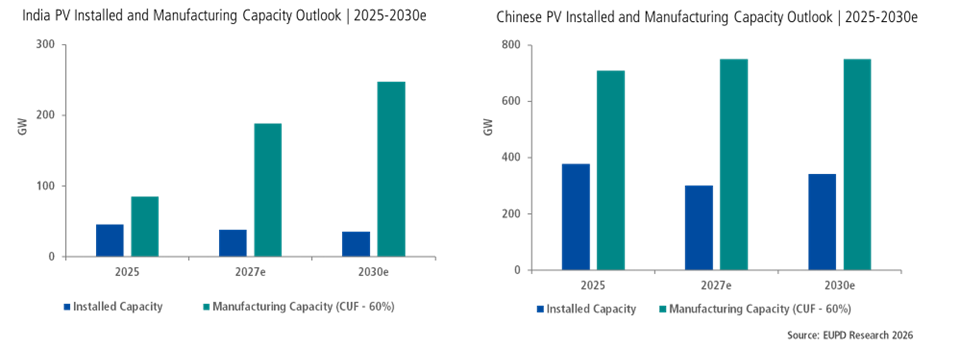

As Europe strengthens its position as a leading demand center for solar and storage, it is also becoming the primary destination for expanding global supply. While China already plays a dominant role in supplying the European market, rapid manufacturing expansion in India is expected to follow, positioning it as the next major export contributor. This dynamic increasingly links global production capacity with European market demand.

In China, PV manufacturing capacity reached approximately 1,180 GW in 2025, translating to around 708 GW assuming a 60% capacity utilization factor (CUF). Output is projected to rise further to approximately 750 GW annually (with a 60% CUF) in the next five years, significantly exceeding domestic installation levels of about 320 GWdc. As domestic installations stabilise under China’s evolving energy planning frameworks and long-term capacity alignment under the 15th Five-Year Plan, this imbalance is expected to sustain a structural export surplus.

India is moving in a similar direction, although at an earlier stage. Supported by production-linked incentives and import duties, domestic manufacturing capacity is expanding rapidly and has exceeded the local demand in 2025. By 2027, export potential is estimated to be around 188 GW, with a CUF of 60%, reinforcing its role as an emerging global supplier.

At the same time, access to the United States remains constrained by tariffs, Foreign Entity of Concern rules, and strict origin requirements, limiting the ability of many Asian manufacturers to compete freely in that market. As a result, a growing share of global solar and storage supply is being redirected toward Europe, further increasing competitive intensity.

This convergence of strong demand and expanding supply is transforming Europe into a filtering market, particularly as demand from C&I applications continues to scale. While the region remains highly attractive, its capacity to absorb excess supply is not unlimited. Instead, intensifying competition is driving greater selectivity, where success depends on meeting evolving buyer expectations around quality, reliability, and long-term performance.

From Volume Growth to Risk-Aware Procurement

As supply intensifies and competition increases, procurement in Europe’s C&I segment is becoming more selective and risk-driven. Insights from EUPD Research’s InstallerMonitor© and C&I EPCMonitor© across leading European markets indicate that purchasing decisions are no longer based on upfront cost alone, but on long-term performance and supplier credibility.

This is reflected in EPC responses, where 53% prioritise premium-quality equipment as a proxy for reliability, 51% emphasise extended manufacturer warranties, and 41% highlight ESG-compliant suppliers as key risk mitigation measures. Notably, over 70% of EPCs indicate a willingness to pay a 10–15% premium for solutions that offer these safeguards. Buyers are therefore prioritising premium-quality equipment alongside suppliers that demonstrate strong ESG compliance and consistent product performance, with extended warranties reflecting the importance of financial resilience and long-term bankability in ensuring system stability.

What It Takes to Win in Europe: A Three-Pillar Approach

As Europe becomes the focal point of both global demand and supply, succeeding in this selective market requires a more structured and adaptive strategy. The convergence of geopolitical volatility, supply pressure, and risk-aware procurement is redefining how suppliers approach market entry and expansion. Three strategic pillars are emerging as critical for long-term success.

- Targeted Market Prioritisation

Not all European markets offer the same level of opportunity, and these differences are becoming more pronounced under current energy conditions. Variations in electricity prices, regulatory frameworks, grid constraints, and segmental demand require a more granular approach to market selection. Addressing this need, EUPD Research is introducing the Market Tierization Workshop© Europe to support structured market prioritisation. The approach evaluates markets across multiple dimensions, including electricity tariffs, LCOE and net benefit of solar and storage, historical and forecast installation trends, the presence of negative electricity pricing, PV per capita indicators, and the evolution of segmental demand across residential, C&I, and utility markets. It also incorporates regulatory frameworks, funding schemes, and downstream indicators such as brand awareness, portfolio presence, and installer recommendations. This enables suppliers to move beyond broad regional strategies and identify markets where growth potential, accessibility, and competitive positioning are best aligned. Importantly, this approach also highlights that even structurally less attractive markets can offer strategic opportunities depending on a company’s positioning, entry stage, and competitive context. - Dynamic Market Intelligence

In a rapidly evolving environment, static market assessments are no longer sufficient. Policy changes, pricing dynamics, and demand signals are shifting too quickly, particularly under ongoing geopolitical uncertainty. Continuous, data-driven market intelligence is therefore essential to track developments and adapt strategies in real time. This requires structured, continuously updated market intelligence covering installations, forecasts, regulatory changes, tender activity, and electricity market dynamics across key regions. EUPD’s Global Energy Transition (GET) Matrix© illustrates how such intelligence can be systematically consolidated across 60 global PV markets and 30 energy storage markets. - Downstream Market Alignment

Finally, success in Europe depends on aligning with downstream market expectations. As procurement becomes more risk-aware, suppliers must respond to the priorities of installers, EPCs, and end customers, who are placing greater emphasis on reliability, bankability, ESG compliance, and system performance. This requires not only strong products, but also a clear positioning that reflects these expectations across the value chain. In this context, EUPD Research’s Brand Leadership and Sustainability Rating© (BLSR) provides a holistic framework to evaluate suppliers across key dimensions, including installer and EPC recommendation, ESG and innovation performance, and financial stability, with the latest evaluation results currently available and the next update expected in the coming weeks.

Together, these three pillars define a more strategic approach to navigating Europe’s solar and storage market. In an environment shaped by volatility and increasing selectivity, companies that combine precise market prioritisation, continuous intelligence, and strong downstream alignment will be best positioned to convert opportunity into sustainable growth.

Conclusion

The current geopolitical tensions reinforce a structural shift already underway in global energy markets, where volatility, supply insecurity, and price uncertainty are accelerating the transition toward solar and storage.

Within this global context, Europe is emerging as the most competitive global destination for solar and storage supply. As manufacturing capacities in China and India continue to expand beyond domestic absorption, and access to alternative markets remains constrained, a growing share of global solar and storage supply is being directed toward Europe. However, the region’s ability to absorb this surplus is not unlimited. Instead, intensifying competition is creating a more selective market environment, where only suppliers aligned with evolving buyer expectations can secure long-term positions.

This shift reinforces the need for a more structured approach to market engagement. As conditions vary across countries and continue to evolve under geopolitical pressure, success depends on prioritising the right markets, adapting to dynamic developments, and aligning with risk-aware procurement strategies.

Ultimately, Europe’s solar and storage market is not only expanding, but becoming more complex and competitive. In this environment, companies that combine targeted market selection, continuous intelligence, and strong downstream alignment will be best positioned to navigate uncertainty and capture sustainable growth.

Authors: Daniel Fuchs and Ali Arfa

Daniel Fuchs is the Chief Customer Officer of EUPD Group. He has extensive international experience in sales, marketing, customer engagement, and strategic event management within the renewable energy and cleantech industries. His work focuses on building customer-centric growth strategies, strengthening global partnerships, and supporting market development across the solar, energy storage, and sustainability sectors. He can be reached at d.fuchs@eupd-research.com.

Ali Arfa is the Head of Data Management at EUPD Research. He is a graduate of the University of Bonn and with a background in European and North American politics. His expertise encompasses market research, policy development, and stakeholder analysis. His particular focus is on solar energy, energy storage, and strategic consultation. He can be reached at a.arfa@eupd-research.com.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Popular content